The card-based payments mechanism has evolved over many decades and is now a commonplace experience for both the consumer and merchants. Recently there has been a steady stream of new payment innovations, though none has yet to achieve the ubiquity of the traditional card. So what near-term changes can we expect in the US market in how consumer payments are conducted? In this paper we will be looking at potential drivers for change, specifically;

From a technology perspective it is reasonable to assume that the necessary ingredients and know-how currently exists to build any form of consumer payments system. Cloud-computing, strong encryption, AI and machine learning, blockchain, crypto-currencies, and digital wallets, are all ingredients for a new era in consumer payments. However, it is not the technology that will ultimately determine the direction of consumer payments but rather who stands to benefit within the payments ecosystem. So who might benefit from a new consumer payments method and who might lose out?

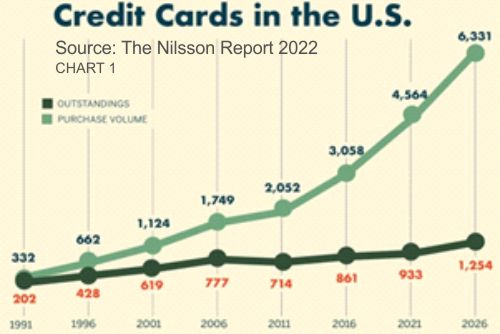

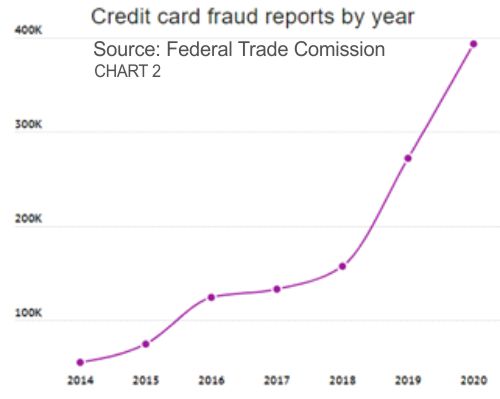

The rampant fraud losses rightfully creates great concern. There is a deep, moral instinct that kicks in when the 'bad-guys' seemingly get away with criminal gains. There is certainly some great AI and machine learning technologies emerging that are creating tangible reductions in fraud levels. However, one of the great challenges of fraud detection and prevention is that fraud evolves. Card fraud is no longer the purview of chancers and petty thieves, it has become the domain of sophisticated, organized crime gangs with the capability to probe security defenses and rapidly exploit any vulnerabilities. The irony is that despite more and more consumers being impacted by card-related fraud the popularity and increased usage of credit cards suggests there are still significant gains to be made by the card processing networks and card issuers. With commercial factors being what they are, card processing organizations are under no obligation to eliminate fraud. Provided that the losses are sufficiently small relative to the financial gains then the quest for more growth becomes the priority. Given the healthy profits associated with card processing and its apparent entrenchment into the commercial fabric it begs the question - “is there sufficient pressure for change?” Consumers who are subjected to card fraud often face significant inconvenience trying to recover lost funds and restore reputations. With the current levels it is reasonable to assume that consumers are becoming increasingly open to alternate payment methods. However, consumer dissatisfaction cannot of itself introduce a new payments option. We need another trigger point. The question of interchange fee rates has been a long running battle between retailers, card issuers, and the networks. Retailers have long held the view that they are being gouged over interchange fees and service charges. In 2021, the Global Payments Consulting firm GMSPI issued a comprehensive report highlighting the dramatic imbalance in commercial profits experienced by the different players in the card-payments chain.

THE CLIENT This Lusis Payments customer is one of the largest financial institutions in the world. The organization has over 10 million global customers covering several public and business sectors. They provide tailored banking solutions for personal, small business, commercial and cross border payments. THE NEED: Freedom from a Constraining Legacy Payments Platform The client's business was becoming severely constrained by their 28 year-old legacy payments system. The high cost of ownership, lengthy development times, and soaring maintenance challenges became urgent pressures for change. The legacy software was widely utilized throughout the client's vast line of banking services. It was therefore crucial that the new solution would provide a highly extensible architecture, facilitate low-risk migration projects, and have the robustness to handle diverse and high-growth volumes. Additional high-priority requirements included;

“We have implemented more “new” functional capabilities in the last 3 years on the TANGO platform than we have in over a decade on our previous legacy platform. It is great to be free from all the constraints.”

|

lUSIS nEWSThe latest company and industry news from Lusis Payments. Archives

June 2024

Categories

All

|

RSS Feed

RSS Feed