By Dave Smith - Consultant, Lusis Payments

It was John Gage of Sun Microsystems who coined the phrase, “the Network is the Computer” - way back in 1984. Understandably, this phrase was originally more of a vision than the reality. However, the ensuing 38 years of computing development has generated incredible progress. With the advent of Cloud computing we now live in a world where on-demand computing infrastructure can be readily purchased and deployed within any geographic region. Surely we can agree that the computer industry has fully delivered Gage’s historic vision. However, putting aside the numerous technical achievements we also need to consider the functionality of the software itself. A recent banking experience provided a sobering reality check and several points to ponder. My “customer journey” started when I needed to update the registered address on my business account. This was accomplished easily enough using the online banking facilities. The real challenges started when I tried to change the address on the associated credit card. I had naively assumed that this could also be done online - given that both my business account and credit card were issued by the same bank. After a lengthy wait in the phone queue, the support agent for the credit card team informed me that the address change for account had not updated on her system yet. Furthermore, it could take up to 3 business days to complete. Additionally, it wasn’t clear whether I would automatically receive a notification message once the credit card address was changed. What!? So much for the “seamless customer journey” ideas that I hear being preached at banking conferences. Today, banks are rightly giving significant attention to their “Cloud Strategy”, whether it be in the planning stages or early implementations. The recent acquisition of Cloud payments specialist, Renovite, by JPMC demonstrates the importance some banks are assigning their Cloud strategies. In my view, a cloud strategy should not become overly distracted by the technology itself. The staggering levels of investment being injected by Microsoft, Google, Amazon, and others, will ensure that the Cloud will consistently become better and better. The real question that banks need to ask themselves concerning their Cloud Strategy is what software investments are required to improve operational efficiencies, streamline the customers’ journeys, and increase competitive agility. Simply shifting the same tired, poorly integrated ‘software blobs’ into the cloud may save a few bucks. It might even win the CIO some Brownie points. But it will do very little to Transform their business. Hopefully, it is the Transformative potential of the Cloud that will guide the banks’ strategies beyond the short term cost gains. Contact Lusis Payments when developing your Cloud strategy for solutions that improve your organization's operational efficiencies and improve customer experiences.  by David Smith As a long serving practitioner in the ATM Industry I have witnessed several policy decisions that really intrigued me. For example, some banks take the stance that their in-branch automation is solely for their own customers. Others, take a more inclusive approach allowing non-bank consumers to use their facilities alongside their own clients. I have certainly experienced both sides of this question in different parts of the world. As a fan of consumer-centric businesses, I favor the latter approach, although I understand the rationale of the “my customers only” principles. However, the policy thinking around “who will you serve?” becomes further convoluted when you recognize that many banks run promotions to attract new customers, offering money to new customers as a signing-up reward. Sometimes these incentive payments can reach £100 or more. Surely, allowing non-bank consumers to use your branch automated services can be a powerful recruitment aid. I mean, you know exactly where they are at that point in time, what they are doing, and you have staff on hand to help and advise them appropriately. Surely this is a good thing, right? Once you truly embrace every consumer interaction as an opportunity to learn something new, to deepen the relationship, then you fundamentally change the possibilities for growth. Traditionally, banking automation was mechanically sophisticated but depended on proprietary vendor software to work. Consequently, banks often faced substantial costs for even simple customizations, particularly if they had a mixture of hardware from different vendors. Under these circumstances it was difficult to personalize the consumer’s experience, or to differentiate yourself from your competitors in a meaningful way. An investment in vendor-independent ATM software ensures true portability across any self-service device, thereby reducing costs and creating a greater choice in hardware. Happily, this restrictive situation has changed significantly with the growing market trust in vendor-independent, multi-vendor, ATM software. Additionally, the ATMIA’s new blueprint architecture clearly separates the task of terminal management from the payments switch, and embraces the versatile ISO 20022 messaging standard instead of the proprietary and more restrictive NDC protocol. These changes eliminate two of the greatest blockers to service flexibility. Banks now enjoy ready access to affordable self-service technologies, freeing them to create any branch experience they want. The next leap forward in ATM channel excellence is the application of relevant, real-time consumer information in a way that benefits both the consumer and the bank. Specifically, this step involves the deployment of workflow orchestration and machine learning-based recommendation engines.

So, how might a bank leverage workflow and recommendation engine technologies to improve their in-branch experience for both their own, and the non-bank, consumers?

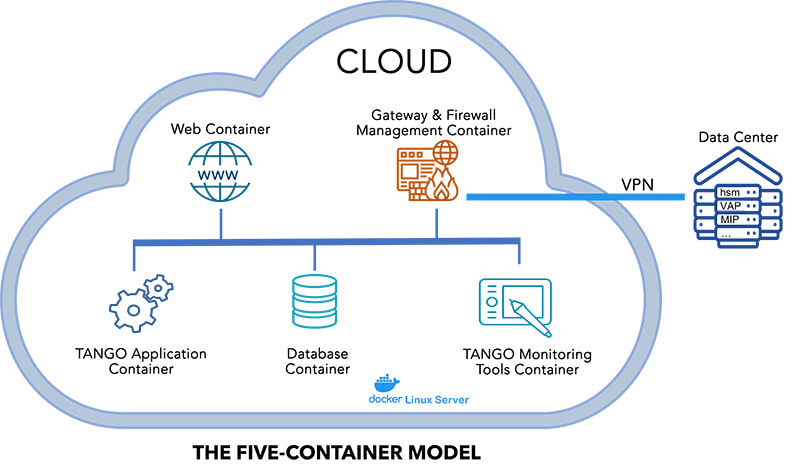

Traditionally, an ATM would collect the card and PIN information before sending any information to the switch. This is all ‘dead-time’ during which the bank has no information about the consumer to act on. In a more consumer-centric approach, the ATM sends the card information to the switch as soon as it is entered. The switch replies with relevant consumer information that can be used to personalize the services offered. In addition, advisory information can be sent to a branch agent’s device notifying them about the consumer, the machine they are using, and what should be done. Furthering this illustrative scenario, the recommendation engine might determine that a non-bank consumer qualifies for an account sign-up special offer or other guest services based on the number of previous visits, the time of day, transactions performed, etc. Special offer vouchers could be dispensed via the receipt printer for redemption with a branch agent. Simple guest services could include the waiving of the acquiring fees in return for phone number information or other contact details. Numerous other relationship-building options can be easily and affordably implemented with today’s technology. The biggest obstacle to the creation of consumer-centric ATM channels used to be the infrastructure but this is no longer true. A much larger obstacle, in my opinion, is the legacy mindset among senior stakeholders that rejects the ATM channel as a vehicle for innovation and richer consumer services. The financial pressures causing banks to close branches on a large scale are highly unlikely to subside any time soon. This situation is further aggravated by regulatory pressures on banks to provide third party access to consumer data – thereby inviting new competition for financial services. Now, more than ever, banks need to focus more about personalizing the consumer experiences they create as a means to strengthen brand loyalty and growth.  TANGO is the world's most performant Retail Payments solution with benchmark tests demonstrating 10,000 transactions per second. Built using a micro-services architecture, TANGO is also feature-rich and easily extensible. Backed by Lusis' proven track record it is not surprising that more and more organizations are swapping out their legacy payments infrastructure for TANGO. TANGO is the culmination of decades of crafted engineering that ensures the maximum operational performance and reliability as well as the most affordable cost of ownership. For example, TANGO includes a Self-Monitoring and Auto-Spawning feature whereby a suite of timers can be configured to monitor the processing time for specific events. By comparing the real-time measurements against the defined norms TANGO can immediately identify bottlenecks as soon as they occur. TANGO can also be configured to automatically spawn new instances of the affected micro-service or process thereby ensuring the required throughput is maintained. TANGO uses the Docker containerization platform and a typical deployment uses the 5-Container model shown below.  Significantly, the container boundaries are defined to simplify manageability. For example, the gateways and firewalls are combined in a single container to simplify PCI certification tasks. Equally, the monitoring and other tools are located in a dedicated container to ease system evolution. This approach has numerous benefits, not least of which is that it is well proven and supports the easy and secure use of cloud infrastructure. However, in this model, container creation is still a manual process. Consequently, Lusis has expanded TANGO's container model to deliver the full elastic scalability advantages of a cloud-native environment.

The card-based payments mechanism has evolved over many decades and is now a commonplace experience for both the consumer and merchants. Recently there has been a steady stream of new payment innovations, though none has yet to achieve the ubiquity of the traditional card. So what near-term changes can we expect in the US market in how consumer payments are conducted? In this paper we will be looking at potential drivers for change, specifically;

From a technology perspective it is reasonable to assume that the necessary ingredients and know-how currently exists to build any form of consumer payments system. Cloud-computing, strong encryption, AI and machine learning, blockchain, crypto-currencies, and digital wallets, are all ingredients for a new era in consumer payments. However, it is not the technology that will ultimately determine the direction of consumer payments but rather who stands to benefit within the payments ecosystem. So who might benefit from a new consumer payments method and who might lose out?

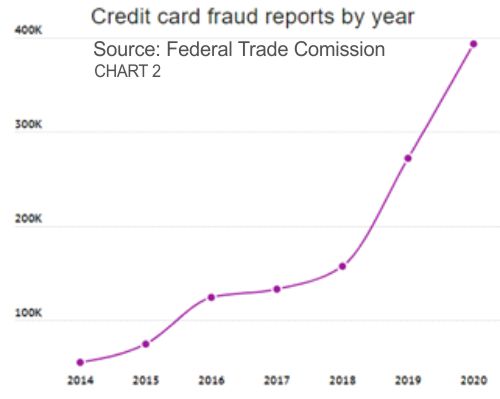

The rampant fraud losses rightfully creates great concern. There is a deep, moral instinct that kicks in when the 'bad-guys' seemingly get away with criminal gains. There is certainly some great AI and machine learning technologies emerging that are creating tangible reductions in fraud levels. However, one of the great challenges of fraud detection and prevention is that fraud evolves. Card fraud is no longer the purview of chancers and petty thieves, it has become the domain of sophisticated, organized crime gangs with the capability to probe security defenses and rapidly exploit any vulnerabilities. The irony is that despite more and more consumers being impacted by card-related fraud the popularity and increased usage of credit cards suggests there are still significant gains to be made by the card processing networks and card issuers. With commercial factors being what they are, card processing organizations are under no obligation to eliminate fraud. Provided that the losses are sufficiently small relative to the financial gains then the quest for more growth becomes the priority. Given the healthy profits associated with card processing and its apparent entrenchment into the commercial fabric it begs the question - “is there sufficient pressure for change?” Consumers who are subjected to card fraud often face significant inconvenience trying to recover lost funds and restore reputations. With the current levels it is reasonable to assume that consumers are becoming increasingly open to alternate payment methods. However, consumer dissatisfaction cannot of itself introduce a new payments option. We need another trigger point. The question of interchange fee rates has been a long running battle between retailers, card issuers, and the networks. Retailers have long held the view that they are being gouged over interchange fees and service charges. In 2021, the Global Payments Consulting firm GMSPI issued a comprehensive report highlighting the dramatic imbalance in commercial profits experienced by the different players in the card-payments chain.

“Do you take plastic?”

There was a time when consumers were asking that question in Retail outlets around the world. Nowadays, the ability to pay for goods and services with a debit or credit card is so commonplace that consumers simply assume that card acceptance is available virtually everywhere. It wasn’t always like this but several decades of investment has built the card payment infrastructure to its current state. However, despite the continued growth in consumer payment transactions, card payments does have its drawbacks. The level of fees paid by merchants has been a long standing area of contention, often resulting to protracted legal action to enforce greater billing transparency and reductions in overall fee costs. Another area of serious concern is the dramatic increase in card and account fraud, clearly aggravated by consumer behavior changes during the pandemic. Of course, the quest for ever simpler and more secure payment options is of great interest to many consumers. There has been a lot of payments innovation over the years including stored value cards, digital wallets, and bio-metric authentication. However, many of these schemes piggyback on the card infrastructure or achieve only limited levels of success. In most industries technology has been reinventing itself at accelerating rates but this is not the case with card payments. This begs the question – “Is the card itself the bottleneck to change?” Putting aside the entire settlement cycle there are several key elements that a truly alternative consumer payments option needs to address. Firstly, the consumer needs to have some form of payment token and authentication method. Additionally, the alternate payment scheme needs to ensure the secure acquisition and routing of the payment to the appropriate institution for authorization. The advent of smartphones and wearable computing, coupled with the growth of real time account to account payments is already proving to be an interesting possible alternative to card payments. Some adoption rate projections suggest that account-based payments could notionally obsolete card-based payments. It seems that the real hurdle to obsoleting card payments is a commercial issue, not a technical one. As long as the new entrants into the consumer payments market all seek their own “magic bullet” then they are most likely to be left nibbling around the market share of the traditional card brands. The last thing consumers want is to be drip-fed an endless array of different payment options with no clear indication of convergence and interoperability. The electric car market provides a great comparison in this regard. In an age of climate change and excessive wastage it seems obvious that governments should demand all electric cars sold in their country to have the same charging connection. The cost and timescales to create an effective charging stations infrastructure is immediately reduced, and consumers would have greater confidence to switch to electric cars. I have no doubt that were the governments of a few of the major market countries to take this bold step it would be universally applauded and the card manufacturers would deliver the requisite standards in a heart beat. The US market saw a strong consortium of banks cooperate in the launch of Zelle as a competitive counter to Venmo. However, the really big question is whether the banks, Fintechs, and Retailers can cooperate to deliver a single, ubiquitous consumer payments option that can move us beyond the 70 years history of plastic cards. |

lUSIS nEWSThe latest company and industry news from Lusis Payments. Archives

June 2024

Categories

All

|

RSS Feed

RSS Feed